CRE “By the Numbers”: Internal Rate of Return (IRR)

In our first installment of “By the Numbers”, we looked at a common metric for return on investment: a property’s capitalization rate or “cap rate.” As we saw there, many factors can influence a property’s cap rate and determining what makes for a “good” rate is often a lot more complicated than just looking for the higher number.

In addition to cap rates, however, there are several other metrics investors and commercial real estate (CRE) professionals can use to determine returns. Another common return metric that can tell you a lot about a property’s investment potential is the Internal Rate of Return or IRR.

IRR defined

Investopedia defines IRR as: A financial metric, used to measure the profitability of an investment, that takes into account the time value of money.

In other words, the IRR metric accounts for the fact that money received earlier is more valuable (given inflation and the potential to generate interest). This also means that, to calculate IRR, you need to have some idea of the cash flows a property will produce each year over the period of investment.

For example, an IRR calculation would include what you initially paid for the property, the amount you expect it to generate in rent each year (which would vary), and the amount you expect to be able to sell the property for later.

The actual equation to calculate IRR is fairly complicated (the Corporate Finance Institute gives an excellent breakdown here) and you’d typically use software or an online calculator to determine it. For the purposes of understanding the importance of this metric to CRE investing, however, it’s more useful to break things down in terms of what IRR tells us about an investment.

IRR essentials

Because IRR considers cash flows on a yearly basis over multiple years, it allows investors to see when they could expect a full return on investment, and how much profit they would make each year thereafter.

Comparing the IRR of two properties can therefore give investors a more nuanced understanding of how each will perform over time, and which is likely to be the better investment. All else being equal, a property investment that generates the same earnings sooner will have a higher IRR.

A “good” IRR?

Importantly, like cap rate, IRR is another metric where simply having a “higher value” doesn’t tell you whether a specific property is a better investment. For example, two properties might have the exact same IRR, but one generates a lot more profit over time than the other. The catch is that those profits are paid out later.

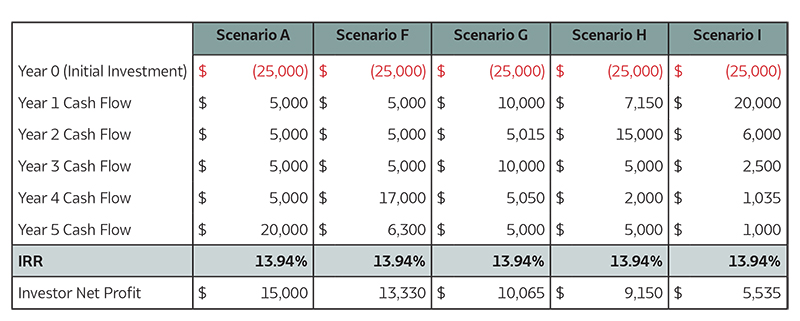

Real estate investment platform ArborCrowd gives a useful example:

(Source: ArborCrowd)

As the above scenarios show, with the same initial investment, but different cashflow horizons, the IRR is the same. The difference between the scenarios lies entirely in when returns are provided, and how much those returns are.

The value of the investment therefore really depends on what the investor’s expectations are. Would they rather wait longer for a bigger payoff, or could short-term gains be put to use in a way that generates more money elsewhere?

As with all things CRE, the exact value that constitutes a good IRR also depends on the sector, and the risk, involved in the investment.

IRR and other metrics

Like many return metrics, IRR can help investors understand specific information about a potential deal. IRR is useful in that it takes into account cash flows generated over multiple years and gives a view of returns on an annualized basis. Worth keeping in mind, however, is that IRR relies on forecasting cash flows (and a potential exit sale price), and many risk factors can affect those valuations in the long run.

By comparison, cap rates provide a “snapshot” of the income a property generates in a year in relation to its current value. It’s a less nuanced metric, but one that can also tell investors something about immediate risk versus reward.

In addition to these two, there are several other metrics the savvy investor should consider. We’ll be examining those in detail in future installments, so be sure to check back for more insight into CRE “By the Numbers.”